Moving day is already emotional enough. The last thing you want is to open a box in your new place and realize something’s broken… or worse, that a box never made it off the truck at all.

If you’re reading this because something went wrong during a move, take a breath. You’re not the first person this has happened to, and you actually have more rights and options than most people realize.

In this guide, I’ll walk you through:

- What to do the *moment* you notice damage or missing items

- How moving claims actually work in the U.S.

- The difference between valuation and insurance (and why that wording matters)

- How to document everything so your claim doesn’t get denied

- Timelines, real expectations, and how companies like United Prime Van Lines handle it in the real world

This isn’t legal advice, just a practical, “here’s how this usually plays out” explanation from the moving side.

In the moving world, a “claim” is any formal request for compensation because:

- Something was damaged

- Something went missing

- Something was delivered late in a way that caused a loss (less common, but it happens)

Most people don’t realize that the claim process actually starts *before* moving day, when you choose what level of protection you want.

That’s where “valuation” and “insurance” come in.

Here’s the part that trips up almost everyone.

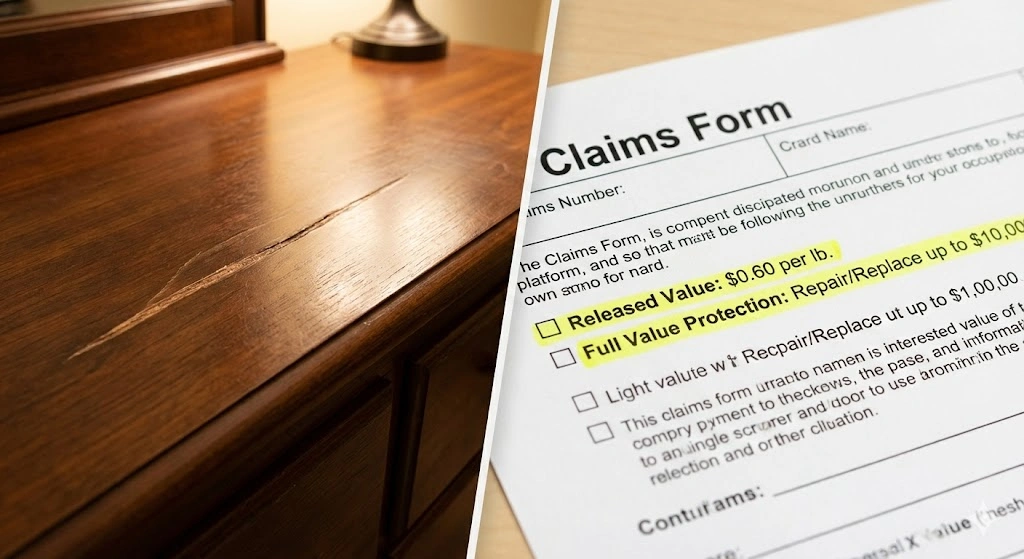

Valuation is the level of liability the moving company agrees to take on for your stuff. It’s regulated by federal law for interstate moves and shows up in your paperwork, usually as two main options:

1. **Released Value Protection (basic coverage)**

- Standard, no extra charge

- Covers up to **$0.60 per pound per article**

- Example: Your 20 lb TV is damaged → 20 lb x $0.60 = $12

- That’s it. That’s what the mover is legally responsible for under this option.

2. **Full Value Protection (FVP)**

- Costs extra

- The mover is responsible for **the current market value** of items that are lost or damaged, up to the amount you declare

- The company can choose to:

- Repair the item

- Replace it with a similar item

- Pay you the current replacement value

When you move with a carrier like United Prime Van Lines for an interstate job, you’ll be offered these options clearly in writing. That choice massively affects what your claim outcome looks like.

Technical but important:

- Movers provide **valuation**, not “insurance” in the traditional sense.

- Some customers also buy **third-party moving insurance** on top of that for extra peace of mind (especially for high-value items like artwork, antiques, expensive electronics).

If you’re not sure what you chose, grab your paperwork and look for:

- “Valuation Statement” or “Liability Options”

- Something that mentions either “Released Value” or “Full Value Protection”

That’s your starting point for any claim.

The best time to catch damage or missing boxes is **during delivery**—while the crew is still there and the truck isn’t empty yet.

Try to:

1. **Be present** (or have someone you trust there)

2. As each box or item comes off the truck, check it against your inventory list

3. Put boxes in the correct rooms to avoid confusion later

4. For obvious damage (a ripped box, crushed corner of furniture, cracked glass):

- Point it out *immediately* to the crew lead

- Take photos *before* they try to fix or move anything else

- Make a note on the **Bill of Lading** or **Inventory Sheet** (more on that shortly)

You are absolutely allowed to walk around, inspect, and ask questions. Any good crew (including the guys and gals working with United Prime Van Lines) expects you to be involved in the walkthrough.

Not everything is visible right away. You might discover:

- A scratched dining table leg once you move it

- Electronics that don’t power on

- Missing items only when you fully unpack

You should:

- Unpack the essentials within the first few days

- Make a basic checklist of anything that’s obviously damaged or missing

- Start your claim process sooner rather than later

Even if you don’t have the full list yet, it’s better to open a claim and add to it than to wait until you remember every single item.

For **interstate moves in the U.S.**, the federal rule (for carriers under FMCSA) is generally:

- You typically have **up to 9 months** from the date of delivery to file a written claim with the carrier.

- The moving company then has:

- **30 days** to acknowledge your claim

- **120 days** to pay, settle, or deny the claim (they can extend with explanation if more time is needed)

That said, don’t wait. Filing early usually makes things easier because:

- Everyone still remembers the move

- The records are fresh

- You’ll get your resolution sooner

Local/intrastate rules vary by state, but most reputable movers (including United Prime Van Lines) follow similar time frames and spell that out in your contract.

When in doubt: check your Bill of Lading or Order for Service, or call the mover and ask:

“What is my time limit to file a claim for this move?”

Think of this as building your case in a calm, clear way. The better you document things, the easier it usually is for a claims department to help you.

You’ll want:

For each damaged item:

- Take **wide shots** showing the whole item

- Take **close-ups** of the damage

- Take a photo of any damaged box/packing materials

- If you have **“before”** photos (listing photos, home pics, social media, etc.), those can help too

For missing items:

- Photograph the **space** where they should be (e.g., empty spot where a dresser should be)

- Screenshot any pre-move photos that show you actually owned that item

Pull together:

- **Bill of Lading (BOL)** – the main contract of the move

- **Inventory sheets** with item tags (for long-distance moves these are standard)

- **Valuation election form** – shows what coverage you chose

- **Estimate** and **final invoice**

On your inventory, pay attention to notations like “SC” (scratched), “D” (dented), “MR” (marred), etc. Those codes show pre-existing conditions the company noted before loading. Claims departments will look at those.

If you have FVP or separate insurance, you may need to show current value:

- Receipts or invoices (email receipts are fine)

- Bank/credit card statements

- Product links or screenshots showing current retail replacement price

Don’t obsess over being perfect here—just be honest and reasonable.

Telling the driver “Hey, this is broken” is good to do in the moment, but it’s **not** the same as filing a claim.

You need to:

1. **Contact the moving company’s office or claims department**

- For a carrier like United Prime Van Lines, they’ll either give you a link to an online claim portal or email you a claim form to fill out.

2. **Submit your claim in writing**

- Email, online portal, or physical mail—whatever they require.

- The important part is that it’s written and contains the details.

Expect to provide:

- Your full name and contact info

- Move date(s)

- Origin and destination addresses

- Order or BOL number

- List of damaged/missing items with:

- Item description

- Inventory tag number (if applicable)

- Type of damage or state “missing”

- Approximate purchase date

- Approximate value

- Photos and any proof of value if needed

If you’re moving with someone like United Prime Van Lines, you can also call and say plainly:

“Hey, I have a few items that were damaged during the move. I want to file a claim. What’s the correct way to submit it so it’s official?”

That sentence alone gets you in the right lane.

This is where expectations really matter. Claims aren’t “you say it’s broken, we write a check” situations. There’s a process.

Claims departments typically look at:

1. **Your valuation choice**

- Released Value → $0.60 per pound per article max

- Full Value Protection → repair, replace, or pay up to declared value

2. **The inventory condition codes**

- If the item was marked with pre-existing damage, that will be taken into account

3. **Photos and description**

- Is the damage consistent with a moving incident (impact, shifting, etc.)?

4. **Weight and item type** (especially under Released Value)

- A 3 lb lamp? Max liability is $1.80 under basic coverage

5. **Exclusions in your contract**

Common examples:

- Items packed by owner (PBO) with no visible damage to the box

- Certain fragile items not professionally packed

- Pressboard/particle board furniture that tends to crumble if stressed

- Items with existing damage

This doesn’t mean you shouldn’t claim those items—it just means outcomes may vary.

Let’s say a 60 lb dresser is scratched and one drawer front is broken.

- Under **Released Value**:

- 60 lb x $0.60 = **$36** maximum

- Under **Full Value Protection**:

- The mover might:

- Pay to have it professionally repaired

- Replace it with a similar used/new dresser

- Offer a cash settlement close to current value

Same damage. Very different results.

When you find a damaged item:

1. **Don’t throw it away yet**

- Claims adjusters may need better photos or, occasionally, an inspection.

- If you toss it, it’s harder to prove what happened.

2. **Don’t repair it immediately (unless necessary)**

- If it’s functional and safe to keep as-is, wait for claim instructions.

- If it’s unsafe (e.g., shattered glass), take detailed photos *first*, then safely dispose—but keep any receipts if you pay for a specialty disposal.

3. **Describe the damage plainly**

- “Top right corner dented” is better than “destroyed.”

- Be specific; it helps everyone.

On Full Value Protection, it’s common for a company to arrange:

- A local furniture repair pro

- A refinisher for wood surfaces

- A glass replacement vendor

Sometimes a repair brings an item back to “pre-move condition” more cost-effectively than replacing it entirely, which is why you’ll see that option come up.

Missing items are handled a bit differently than damaged ones.

Best case scenario.

- Stop the crew lead and say:

“Box #43 marked ‘Kitchen’ is on the inventory list but I don’t see it here.”

- Have them **recheck the truck** and the house.

- Note the missing item/box directly on the **inventory** or **BOL** before signing.

This, more than anything, strengthens your claim later because it shows the item wasn’t found at destination.

Sometimes boxes get:

- Delivered to the wrong room

- Stacked behind other boxes

- Mis-labeled

Before assuming something is truly missing:

1. Go room by room calmly and check labels.

2. Verify against your inventory tags if you have them.

If it’s truly missing:

- Add it to your claim as “missing”

- List what you believe was inside the box (be honest—claims people can tell when a “misc kitchen box” suddenly becomes a treasure chest worth $3,000)

Again, your coverage choice (basic vs. full value) will determine how the missing box is compensated.

Once your claim is submitted:

1. **You get an acknowledgment**

- Usually by email, sometimes by mail.

- This confirms they received your claim and starts the clock.

2. **They may ask follow-up questions**

- Additional photos

- Clarification on dates, purchase info, or what exactly you’re asking for

- For higher-value items, they might request more proof

3. **They evaluate and propose a settlement**

- This might be:

- A repair service

- A replacement item

- A cash offer

- Under Released Value, don’t be surprised if your payout feels low—it’s tied to weight, not price.

4. **You can accept or negotiate**

- If something feels off, you can politely say:

“Can you explain how you arrived at that amount?”

- Sometimes there’s room to adjust, especially if new information clarifies value or condition.

Companies that take care of their reputation—United Prime Van Lines included—have a reason to handle claims fairly. They want you telling your friends, “Yeah, something went wrong, but they made it right.”

Here are some real-world expectations to keep in mind.

Moves are rough on furniture. It’s realistic to see:

- Minor scuffs on the undersides of furniture

- Small nicks that could plausibly have been there before

Claims departments will look at:

- Age and material of the item

- Pre-existing notations

- Severity and visibility of damage

A deep gouge on the front of a table? More likely to be considered for compensation. Tiny scuffs on the bottom of a leg? Maybe not.

Pressboard/flat-pack furniture (think budget bookcases and desks):

- Often doesn’t survive disassembly/reassembly or heavy weight shifts

- Many contracts explicitly limit liability on these because of how they’re built

If your $79 particle board shelf crumbled, it’s worth a claim, but don’t expect the same outcome as a solid wood dresser that broke.

Tricky area.

If a TV or soundbar looks perfect but won’t power on:

- Claims folks try to determine if it’s move-related or coincidental failure

- If the item is older, that may work against a full payout

- Sometimes they’ll request a repair estimate or inspection

If you had Full Value Protection and professional packing, your chances are generally better than if you packed it yourself in reused boxes and basic coverage.

No one wants to go through claims twice. A few things you can do on your *next* move:

- **Choose your coverage intentionally**

- If you have a lot of high-value or sentimental items, give Full Value Protection a serious look. It’s not just a checkbox—it changes everything if something goes wrong.

- **Take pre-move photos**

- Quick walk-through videos of your furniture and electronics can be gold later.

- **Let the movers pack fragile/high-value items**

- When we (speaking as a moving company side) pack it, we’re generally more confident defending and compensating if something goes wrong.

- **Ask questions up front**

- “How does your claim process work if something is broken?”

- “What’s covered under this valuation option?”

When you’re working with a company like United Prime Van Lines, the crew and office both want you to understand this ahead of time. It’s much smoother for everyone if you go into move day knowing exactly what will happen if things aren’t perfect.

If you’re currently staring at a broken table leg or a missing box, use this as your straight-to-the-point checklist:

1. **Take photos or videos** of the damage or the empty space where something should be.

2. **Collect your move paperwork** (BOL, inventory, valuation election).

3. **List every item** that’s damaged or missing with basic details.

4. **Contact the moving company’s office or claims department** and ask how to submit a written claim.

5. **Submit your claim** with photos and details as early as you can.

6. **Wait for acknowledgment**, then answer any follow-up questions they have.

7. **Review the settlement offer** and ask for clarification if something doesn’t make sense.

You don’t have to be a lawyer or an expert in moving law. You just have to be organized, honest, and timely.

And if you’re planning a move and want a carrier that doesn’t disappear when something goes sideways, that’s where working with a professional outfit like United Prime Van Lines really makes a difference. We can’t promise every move will be 100% incident-free—but we can promise there’s a real process, real people, and a real effort to make it right if something does go wrong.